Sun TV (NSE:SUNTV)

(Disclosure: Invested. Not a recommendation).

CMP: ₹ 440.65/share

In the past month, I added two new stocks to my portfolio but didn't find the time to write about them. One of them was Bhansali Engineering (BEPL) that I bought for ₹ 92/share. It has since run up over 40% so it doesn't make much sense to write about it now. The other is Sun TV, which I bought for an average price of ₹ 407.5/share and believe is trading at an excellent price for long-term investors.

Brief Overview of Company

Sun TV Network Ltd., part of the Sun Group, is one of the largest media conglomerates in the country. The group operates an array of 33 television channels, reaching over 140+ million households in India and spanning regions across the globe, including the U.S.A, Canada, Europe, Singapore, Malaysia, Sri Lanka, South Africa, Australia, and New Zealand.

The Network produces and broadcasts satellite television and radio software programming primarily in the regional languages of South India, including Tamil, Telugu, Kannada and Malayalam. As it continues to expand its footprint, Sun TV Network has also ventured into the Marathi and Bengali language market with two new channels.

Alongside its TV channels, the Sun Group also operates 69 FM Radio Stations, three Daily Newspapers, and six Magazines. Dinakaran, one of its newspapers, is a leading Tamil daily with daily sales of over 1.4 million copies. Sun Direct, the group's Direct To Home (DTH) Satellite TV service, is one of the largest in India, boasting more than 16+ million subscribers. The Network also manages an OTT platform, “SUNNXT”.

Beyond traditional media, It also operates the Indian Premier League (IPL) franchise “Sun Risers Hyderabad” (SRH) in India and Sun Risers Eastern Cape (SREC) in South Africa.

With its 33 Television Channels in 6 languages, large DTH service provider, 69 FM Radio Stations, 3 Daily Newspapers, 6 Magazines, and IPL franchise, SUN TV stands as a true media powerhouse in India and is currently available at attractive valuations.

How does SUNTV make money?

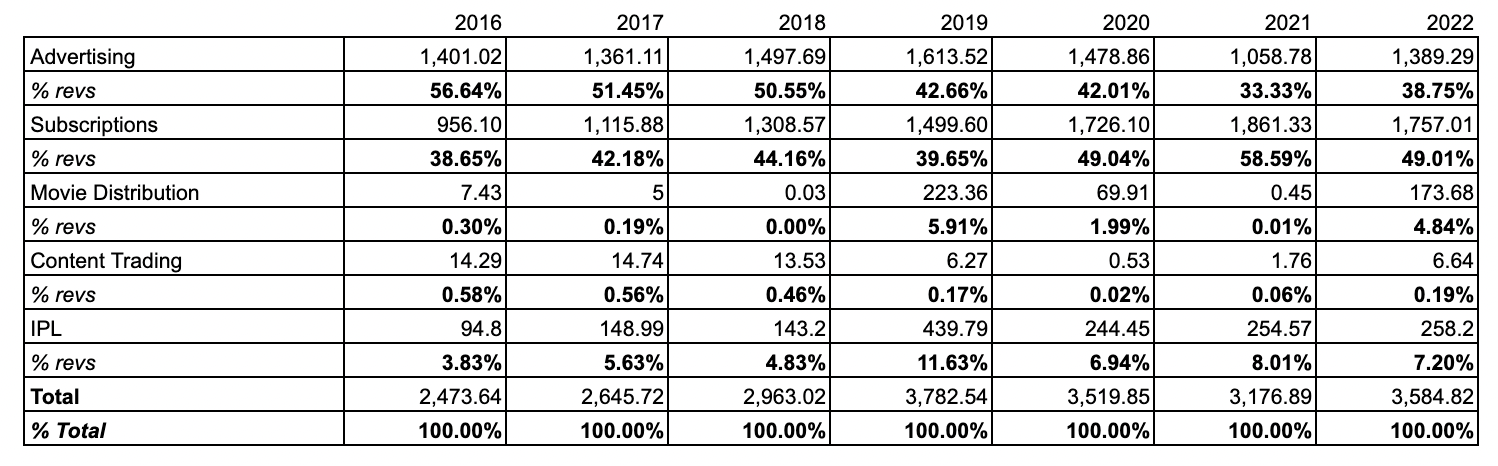

Sun TV makes the bulk of its revenues from advertising and the sale of broadcast slots alongside subscription revenues from its DTH and OTT platform. Together, they account for between 80-95% of revenues each year. The rest of their income comes from movie distribution (which is both highly erratic and volatile), content trading and from the Indian Premier League. Below is a breakdown of their revenues over the last 7 Financial Years (FY16-FY22) and how much each segment contributes to total revenues.

Since both advertising and subscription revenues contribute the bulk of Sun TVs revenues, it might help to view them together. Below is the combined advertising and subscription revenue figures over the same period and their combined contribution to total revenues.

A few trends to note:

- Advertising revenues saw a sharp decline following FY19, dropping from a peak of ₹ 1613cr to as low as ₹ 1058cr in FY21. It rebounded slightly in FY22 to ₹ 1389cr but is still a far shout from the kind of numbers it brought in prior years.

- Subscription revenues had nearly doubled over the last 6 years from ₹ 956cr in FY16 to ₹ 1861cr in FY21, but has since fallen to ₹ 1757cr in FY22.

- Subscription revenues overtook advertising as the lead segment in FY20.

- Movie distribution revenues are volatile, but in certain years (presumably when the group produces box-office hit movies) can contribute a decent amount to revenues. There has been greater contribution to total revenues from this segment since 2019. FY22s figures came off the back of three blockbuster titles features box office icons). For FY23, the box office success Beast starring Vijay, was produced by Sun TV.

- IPL revenues are growing.

- Combined advertising and subscription revenues have trended upwards, though they saw a minor decline in FY21 and have since rebounded.

- Combined advertising and subscription revenues’ contribution to total revenues is trending downwards, with greater contributions coming from the movie distribution and IPL segments. Management believes that the coming years will see a ‘substantial rise’ in revenue contribution from their Cricket Franchises (SRH and SREC) as well as incremental revenues from their DTH and movie distribution segments.

Some management quotes from the FY22 annual report that might be relevant here (I have bolded for added emphasis):

- “In the recent years, subscription revenues have overtaken advertisement revenues, however as mentioned herein with increased viewership, the bandwidth to widen the advertisement revenue base remains very strong. With the continued influence of digitalisation on the Media and Entertainment Industry, the opportunities to enhance the revenue are on the rise.”

- “Sun Network delivers a steady flow of highly popular programs and a dominant share of audience viewership which has given the network tremendous pricing power vis-a-vis competitors.”

- “In the coming years it is expected that the contribution of revenues from the Cricket Franchise will rise substantially further supported by incremental revenues from movie distribution.

- “It is expected that the new stream of revenue for the Company arising from the increased DTH subscriber base in South India would maintain a positive momentum in the coming years.”

With Sun TVs revenue sources out of the way, lets consider whether the company truly has a moat.

What’s SUN TVs moat?

Unless you’re entirely new to the world of investing, you’ve probably heard about company moats. Simply put, a moat (in investing terms), as popularised by Warren Buffett and Charlie Munger, is a sustainable competitive advantage that a business possesses, which protects it against competitors. Moats make a company difficult to compete with and often lead to long-term profitability and market leadership.

Without wasting too much time here, I’ll summarise why I believe Sun TV has a moat, and a strong one at that: